》Check SMM aluminum product quotes, data, and market analysis

》Subscribe to view historical prices of SMM metal spot cargo

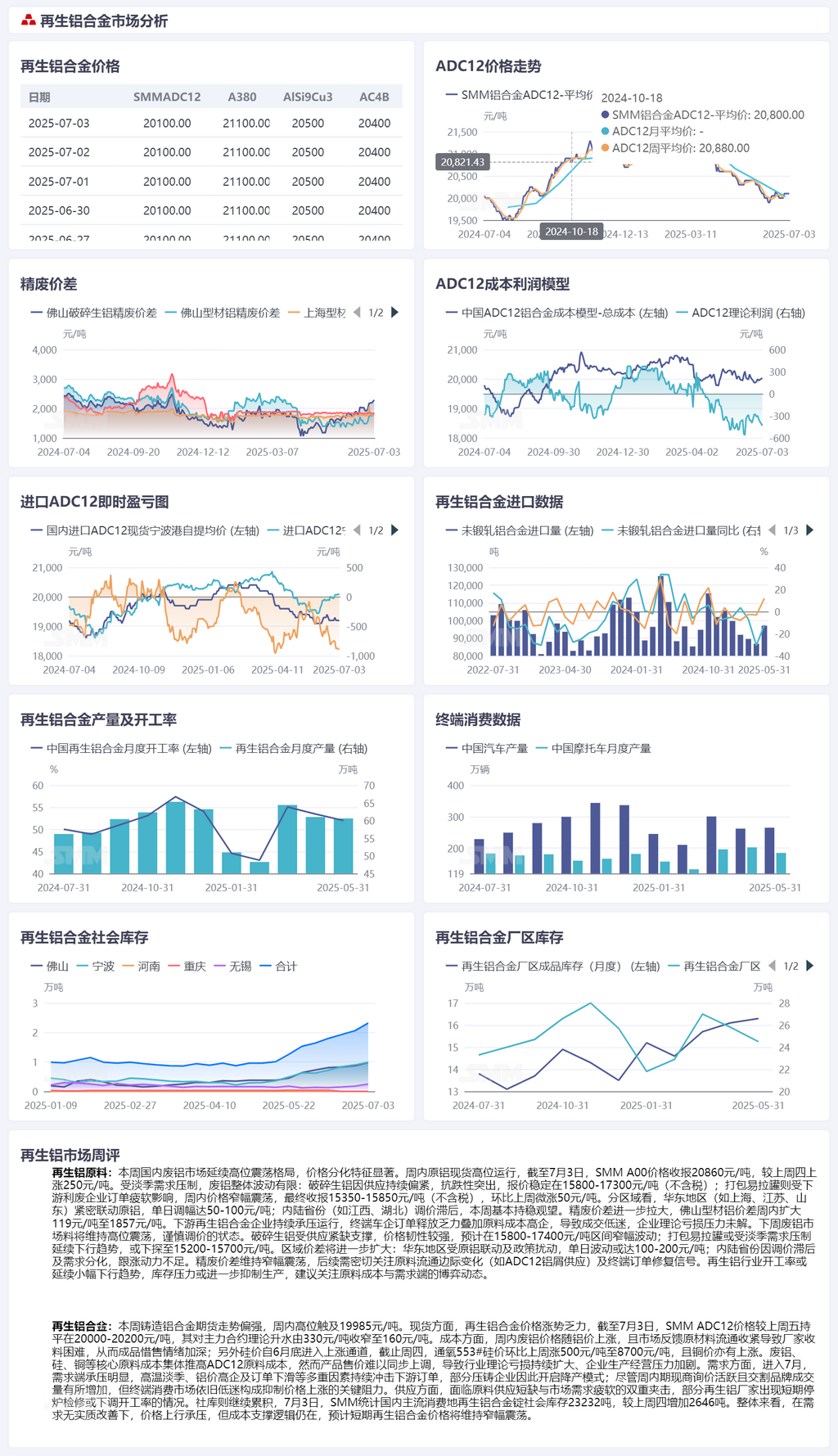

Secondary aluminum raw materials:

This week, the domestic aluminum scrap market continued to fluctuate at highs, with significant price differentiation. Spot primary aluminum prices fluctuated at highs during the week. As of July 3, the SMM A00 aluminum ingot prices closed at 20,860 yuan/mt, up 250 yuan/mt from last Thursday. Due to off-season demand suppression, the overall fluctuation of aluminum scrap was limited: shredded aluminum tense scrap, with its supply remaining tight, showed strong resilience against price drops, with quotes stable at 15,800-17,300 yuan/mt (tax not included). Baled UBC, affected by weak orders from downstream scrap utilization enterprises, experienced rangebound fluctuations during the week, ultimately closing at 15,350-15,850 yuan/mt (tax not included), up 50 yuan/mt WoW. By region, east China (such as Shanghai, Jiangsu, Shandong) closely followed primary aluminum prices, with daily adjustments ranging from 50-100 yuan/mt. Inland provinces (such as Jiangxi, Hubei) had delayed price adjustments and remained basically stable this week. The price difference between A00 aluminum and aluminum scrap further widened, with the price difference of mixed aluminum extrusion scrap free of paint in Foshan expanding by 119 yuan/mt during the week to 1,857 yuan/mt. Downstream secondary aluminum alloy enterprises continued to operate under pressure, with weak order releases from terminal automakers and high raw material costs leading to sluggish transactions. The theoretical loss pressure of enterprises remained unresolved.

Next week, the aluminum scrap market is expected to maintain a state of fluctuating at highs and cautious price adjustments. Supported by tight supply, shredded aluminum tense scrap prices are expected to remain resilient, fluctuating rangebound within the 15,800-17,400 yuan/mt range. Baled UBC may continue its downward trend due to off-season demand suppression, possibly dropping to 15,200-15,700 yuan/mt. Regional price differences will further widen: east China, affected by primary aluminum price linkage and policy disturbances, may experience daily fluctuations of 100-200 yuan/mt. Inland provinces, due to delayed price adjustments and differentiated demand, lack the momentum to follow price increases. The price difference between A00 aluminum and aluminum scrap will remain rangebound, and subsequent attention should be paid to marginal changes in raw material circulation (such as the supply of ADC12 aluminum shavings) and signals of terminal order recovery. The operating rate of the secondary aluminum industry may continue its slight downward trend, and inventory pressure may further suppress production. It is recommended to pay close attention to the dynamics of the competition between raw material costs and demand side.

Cast aluminum alloy:

This week, the futures market for cast aluminum alloy showed a strong upward trend, reaching a high of 19,985 yuan/mt during the week. In the spot market, the price increase of secondary aluminum alloy was sluggish. As of July 3, the SMM ADC12 price remained unchanged from last Friday at 20,000-20,200 yuan/mt, with its theoretical premium against the most-traded contract narrowing from 330 yuan/mt to 160 yuan/mt. On the cost side, aluminum scrap prices rose along with aluminum prices during the week, and market feedback indicated that tightened raw material circulation made it difficult for manufacturers to source materials, deepening their reluctance to sell finished products. Additionally, silicon prices entered an upward channel since the end of June. As of Thursday, the price of oxygen-blown #553 silicon rose by 500 yuan/mt WoW to 8,700 yuan/mt, and copper prices also increased. The collective rise in costs of core raw materials such as aluminum scrap, silicon, and copper has driven up the cost of ADC12 raw materials. However, it has been difficult to synchronously raise product selling prices, leading to a continuous expansion of theoretical losses in the industry and intensified pressure on enterprise production and operation. Demand side, entering July, the demand side has been under significant pressure. Multiple factors such as the high-temperature off-season, high aluminum prices, and declining orders have continued to impact downstream orders, prompting some die-casting enterprises to initiate production reduction modes. Despite active inquiries from futures and spot traders during the week and an increase in trading volume of delivery brands, the end-use consumption market remains sluggish, posing a key resistance to price increases. Supply side, facing the dual challenges of raw material supply deficits and weak market demand, some secondary aluminum producers have resorted to short-term furnace shutdowns for maintenance or reduced their operating rates. Social inventory continues to accumulate. On July 3, SMM reported that the social inventory of secondary aluminum alloy ingots in major domestic consumption areas stood at 23,232 mt, an increase of 2,646 mt from Thursday of the previous week. Overall, in the absence of substantial improvement in demand, prices encounter resistance in rising, but the cost support logic remains intact. It is expected that secondary aluminum alloy prices will maintain a rangebound fluctuation in the short term.